In-flight Entertainment & Connectivity Market Growth to Reach USD 8.2 Billion by 2034 Amid Rising Connected Cabin Demand

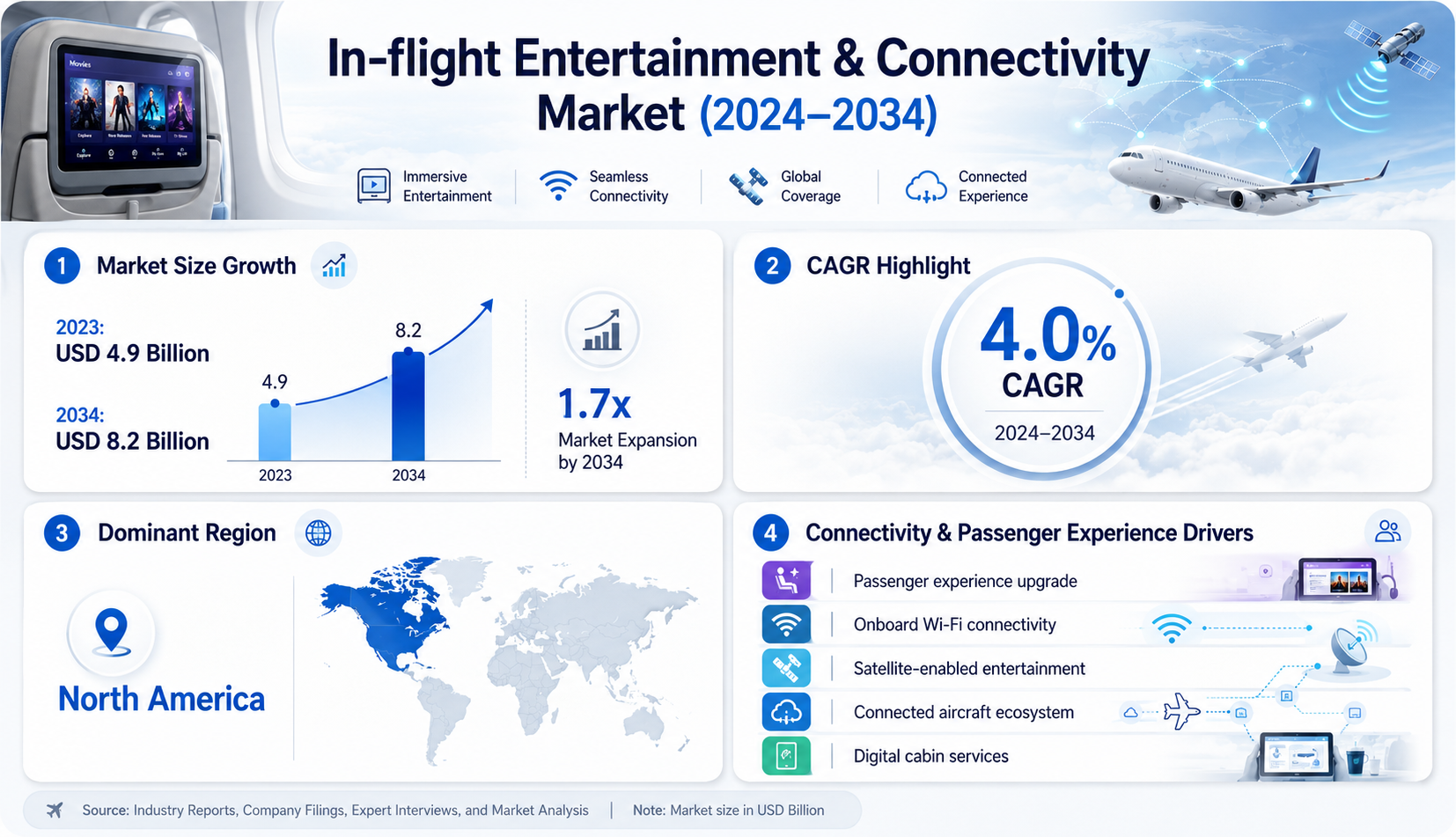

The In-flight Entertainment & Connectivity Market was estimated at USD 4.9 billion in 2023 and is likely to reach USD 8.2 billion in 2034. The In-flight Entertainment & Connectivity Market is expected to grow at a CAGR of 4.0% during 2024-2034. Growth is tied to airline focus on passenger experience and connected cabin services.

IFEC has become more than an entertainment layer; it supports browsing, messaging, content access, e-commerce, live streaming, gaming, and wireless media. Airlines and suppliers are using these services to manage the broader in-flight journey. That makes In-flight Entertainment & Connectivity Market growth closely linked to passenger satisfaction strategies.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/inflight-entertainment-&-connectivity-market#form

Market Segmentation Analysis

The In-flight Entertainment & Connectivity Market is segmented by Aircraft Type into Narrow-Body Aircraft, Wide-Body Aircraft, Regional Aircraft, and Business Jet. Wide-body aircraft is likely to be the fastest-growing aircraft type in the years to come, driven by increasing IFEC penetration and greater relevance on long-haul routes.

By Product Type, the market is segmented into Hardware, Connectivity, and Content. Connectivity is estimated to be the dominant product in the forecast year and is likely to grow at the fastest pace during the forecast period. This highlights the shift toward seamless access rather than hardware-heavy cabin entertainment models.

By End-User Type, the market is segmented into OE and Aftermarket. OE remains dominant in the market over the next ten years and will be the fastest-growing market in the forecast year. New aircraft installations support growth as airlines prioritize advanced IFEC systems at the aircraft delivery stage.

By Sales Channel Type, the market is segmented into BFE and SFE. BFE is to be the dominant as well as the fastest-growing segment by 2034. This reinforces the role of buyer-furnished equipment in shaping IFEC adoption, especially where airline-specific cabin experience requirements matter.

Regional Market Insights

North America is the biggest market. The region’s leadership is supported by high aircraft connectivity penetration, large connected fleets, and the presence of key vendors such as Panasonic, Viasat, Astronics, and Gogo. This gives North America a strong role in the competitive landscape.

Asia-Pacific will be the fastest-growing region by 2034. Rising IFEC adoption in emerging economies such as India, along with increasing air travel demand, supports regional growth trends. The region’s demand profile reflects a direct link between passenger growth and connected cabin investment.

Emerging Trends Shaping the In-flight Entertainment & Connectivity Market

The market outlook is being shaped by BYOD-focused IFEC models. Passenger-owned devices are becoming central to how airlines deliver entertainment, internet access, menu browsing, and retail catalog engagement. This reduces dependence on traditional seatback systems while strengthening personalization opportunities.

Advanced lightweight IFEC systems are also influencing strategic insights across the aviation value chain. These systems enable cost-effective installations and help reduce aircraft weight. As airlines focus on passenger experience and operating efficiency, lightweight connectivity platforms create a practical adoption pathway.

Key Growth Drivers of the Market

• Increasing penetration of IFEC systems is strengthening demand across wide-body aircraft and other aircraft platforms.

• Rising long-haul and ultra-long-haul travel is creating greater need for in-flight passenger engagement.

• Connectivity solutions are helping airlines offer seamless entertainment while managing hardware-related cost pressures.

• BYOD-focused services are improving accessibility by allowing passengers to use familiar personal devices.

• OE installation demand is increasing as airlines prioritize advanced systems on new aircraft.

Competitive Landscape

Top Companies in the Market

Panasonic Avionics Corporation

Gogo Inc.

Intelsat S.A.

Thales Group

Viasat, Inc

Conclusion and Strategic Outlook

The In-flight Entertainment & Connectivity Market is positioned for measured but durable growth through 2034. With a forecast value of USD 8.2 billion and a 4.0% CAGR during 2024-2034, the market’s strategic direction is shaped by connectivity, BYOD adoption, wide-body aircraft demand, and OE installation momentum.

FAQs – In-flight Entertainment & Connectivity Market

What is the forecast value of the In-flight Entertainment & Connectivity Market?

The In-flight Entertainment & Connectivity Market is likely to reach USD 8.2 billion in 2034. It was estimated at USD 4.9 billion in 2023.

What CAGR will the market register?

The market is expected to grow at a CAGR of 4.0% during 2024-2034. This CAGR reflects steady aircraft connectivity adoption.

What are the key growth drivers?

Key drivers include rising air travel demand, wireless connectivity advancements, BYOD solutions, and lightweight IFEC systems. Long-haul travel also increases the value of passenger engagement tools.

Which region is expected to grow fastest?

Asia-Pacific will be the fastest-growing region by 2034. Growth is supported by rising IFEC adoption in emerging economies such as India.

What is the strategic investment outlook?

The outlook favors companies aligned with connectivity, lightweight systems, and aircraft integration. Demand will remain tied to airline priorities around passenger experience and cost-effective cabin technology.