Fuel Cell Catalyst Layer Market Growth to Reach USD 5.6 Billion by 2035 Amid Clean Energy Expansion

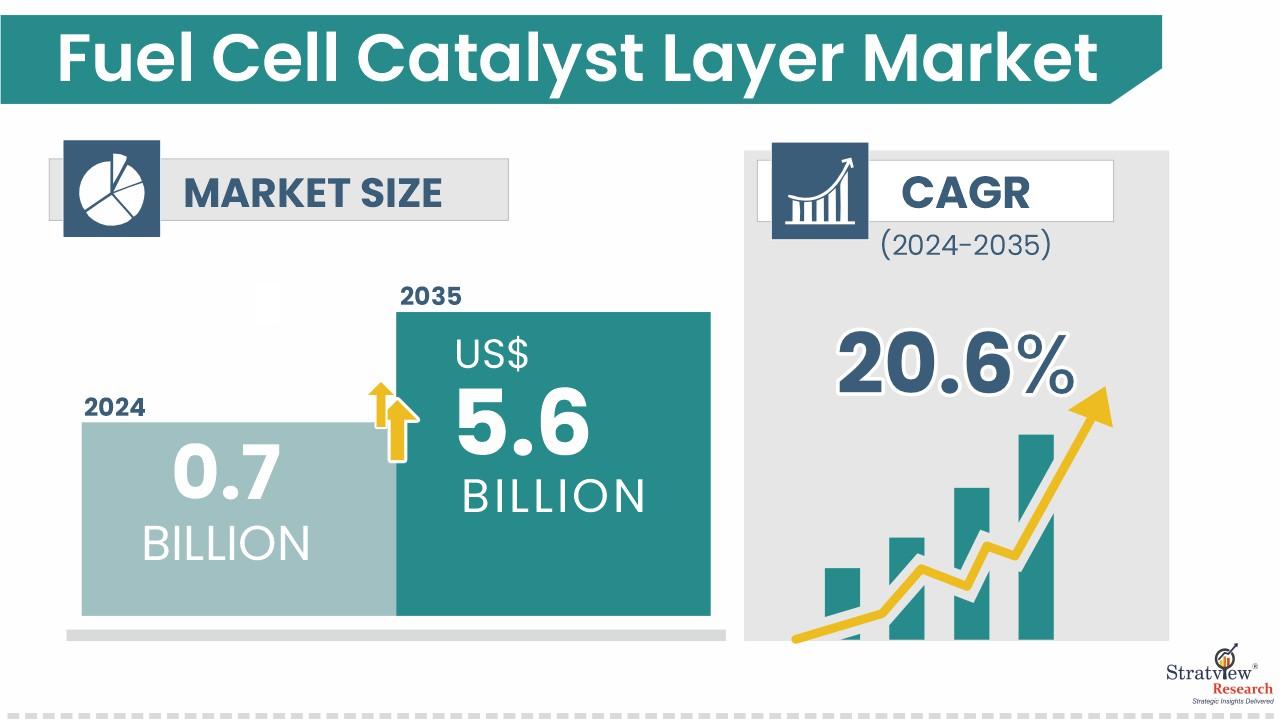

The Fuel Cell Catalyst Layer Market was estimated at USD 0.7 billion in 2024 and is likely to reach USD 5.6 billion in 2035. The market is likely to grow at a CAGR of 20.6% during 2024-2035. The Fuel Cell Catalyst Layer Market is expected to grow at a CAGR of 20.6% during 2024-2035. Demand is rising with alternative technologies to conventional mobility and energy choices.

From a growth analysis perspective, Fuel Cell Catalyst Layer Market growth is tied to the layer’s role in fuel cell efficiency, electricity generation, and durability. The catalyst layer supports the fuel breakdown process and enables reduction and oxidation reactions. Request a free sample report: https://www.stratviewresearch.com/Request-Sample/fuel-cell-catalyst-layer-market#form

Market Segmentation Analysis

The Fuel Cell Catalyst Layer Market is segmented by Fuel Cell Type (PEMFC (Proton Exchange Membrane Fuel Cell), SOFC (Solid-Oxide Fuel Cell), PAFC (Phosphoric Acid Fuel Cell), MCFC (Molten-Carbonate Fuel Cell), DMFC (Direct Methanol Fuel Cell), and AFC (Alkaline Fuel Cells)), by Application Type (Transportation, Stationary, and Portable), by Base Material Type (Platinum-based, Palladium-based, Non-precious Metal Catalysts, and Other Base Materials), and by Region.

By Fuel Cell Type, PEMFC (Proton Exchange Membrane Fuel Cell) is anticipated to propel demand in the catalyst layer market. Its extensive use in transportation, portable, and stationary power applications supports the market outlook. PEMFC benefits such as high power density, rapid startup, and operational flexibility reinforce demand for advanced catalyst layers.

By Application Type, Transportation is expected to be the largest application employing the catalyst layer. Fuel cells in mobility are contributing to market expansion because hydrogen fuel cell vehicles depend on catalyst layers for efficiency and durability. Passenger cars, buses, trucks, and trains create a clear cause-and-effect demand pathway for catalyst layer technologies.

By Base Material Type, Platinum-based materials have dominated the market in the past and will continue to reign in the forecast period. They offer high mechanical strength, excellent conductivity, relatively long life, high catalytic activity, and fast reaction kinetics. Their cost remains a challenge, which is why players are working on alternatives in Non-precious Metal Catalysts.

Regional Market Insights

Asia-Pacific is expected to maintain its reign over the forecast period. The region is supported by fuel cell technology adoption, favorable governments, and evolving hydrogen infrastructure. China, Japan, and South Korea are heavily investing in hydrogen FCEVs, stationary fuel cells, and renewable power initiatives, making the region the primary center of catalyst layer demand.

Asia-Pacific is projected to experience the highest market growth. China is increasing hydrogen production and fuel cell bus and truck deployment. South Korea’s hydrogen economy plans and Japan Hydrogen Society Roadmap strengthen the regional market intelligence view. Enhanced technological advancements and mass production are expected to keep Asia-Pacific ahead in the coming years.

Emerging Trends Shaping the Fuel Cell Catalyst Layer Market

A key industry trend is the move from high-cost precious metals toward material innovation. Non-precious Metal Catalysts are emerging as alternatives to platinum-based materials. At the same time, platinum-based catalysts remain important due to their performance advantages, especially in PEMFC systems used by the automotive industry.

Another trend is the alignment of catalyst layer development with green hydrogen, renewable energy, and fuel cell-based electricity generation. Recent market activity is driven by advanced materials, supply chain strengthening, and cost reduction. Product development around stable electrocatalysts and platinum-magnesium catalyst materials reflects the industry’s focus on improved efficiency and lifespan.

Key Growth Drivers of the Market

- Alternative technologies to conventional mobility and energy choices are increasing fuel cell adoption, which raises demand for catalyst layers.

- Demand for clean energy is expanding the role of fuel cells, creating direct growth trends for catalyst layer applications.

- Advancements in material technology are improving efficiency and durability, strengthening the strategic insights around catalyst layer innovation.

- Supportive government policies and green hydrogen economy objectives are accelerating hydrogen fuel cell adoption and related market demand.

- Renewable energy and fuel cell-based electricity generation investments are increasing the need for catalyst layers as essential energy-system components.

Competitive Landscape

Top Companies in the Market

Johnson Matthey

Umicore

BASF SE

3M

Huntsman International LLC

Heraeus Holding

Haldor Topsoe

Clariant

Tanaka Holdings Co., Ltd.

Ballard Power Systems

Plug Power Inc.

Nisshinbo Holdings Inc.

De Nora

Fuel Cells Etc

Sunrise Power

Conclusion and Strategic Outlook

The Fuel Cell Catalyst Layer Market is positioned for strong expansion, moving from USD 0.7 billion in 2024 to USD 5.6 billion by 2035. A CAGR of 20.6% reflects demand from clean energy, hydrogen fuel cells, transportation, stationary power, and material technology advancements. Asia-Pacific remains central to regional analysis. The strategic outlook is defined by performance improvement, material cost reduction, and scalable fuel cell adoption.

FAQs – Fuel Cell Catalyst Layer Market

What is the Fuel Cell Catalyst Layer Market forecast?

The Fuel Cell Catalyst Layer Market is likely to reach USD 5.6 billion in 2035. It was estimated at USD 0.7 billion in 2024.

What CAGR will the Fuel Cell Catalyst Layer Market record?

The Fuel Cell Catalyst Layer Market is likely to grow at a CAGR of 20.6% during 2024-2035. This growth reflects rising demand for catalyst layers in fuel cell technologies.

Why is the Fuel Cell Catalyst Layer Market growing?

The market is growing due to clean energy demand, advancements in material technology, supportive government policies, and hydrogen fuel cell adoption. Green hydrogen objectives and renewable energy investments further support demand.

What region shows the strongest demand in the Fuel Cell Catalyst Layer Market?

Asia-Pacific shows the strongest demand and is expected to maintain its reign over the forecast period. China, Japan, and South Korea are key demand centers due to hydrogen FCEVs, stationary fuel cells, and renewable power initiatives.

What challenges could affect the Fuel Cell Catalyst Layer Market?

High production costs associated with platinum group metals remain a major challenge. Complex manufacturing, inadequate hydrogen infrastructure, raw material shortages, and competition from lithium-ion batteries may also affect the investment outlook.